Impact of One Big Beautiful Bill on Your Healthcare

TL/DR –

The One Big Beautiful Bill Act (OBBBA), signed into law by President Trump on July 4, 2025, introduces substantial changes to the US healthcare system, including Medicaid, Medicare, and the Affordable Care Act (ACA) coverage. The legislation, which introduces new work requirements and stricter eligibility checks for Medicaid, will affect how people obtain and maintain health insurance, with estimates suggesting that millions could lose coverage in the next decade. The timeframe for most changes introduced by the OBBBA is between 2026 and 2028, and the law also includes provisions for healthcare-related tax-advantaged accounts.

“`html

![]()

The Impact of the One Big Beautiful Bill Act on US Healthcare

Historical reforms in the United States’ healthcare system were brought forth on July 4, 2025, with President Donald Trump’s enactment of the One Big Beautiful Bill Act (OBBBA). Spanning across Medicaid, Medicare, the Affordable Care Act (ACA) coverage, and employer-sponsored benefits, the effects of these changes are far-reaching.

With these modifications, some individuals may encounter new stipulations to retain their health insurance, while others could enjoy expanded flexibility via tax-advantaged accounts. Grasping the nature of these changes and their implementation timeline can aid in preventing unexpected healthcare costs and interruptions in coverage, as recommended by GoodRx, a platform for medication savings.

Key Details of the One Big Beautiful Bill Act

- The OBBBA introduces significant modifications to Medicaid. These include the introduction of work requirements, stricter eligibility checks, and new copays for cost-sharing.

- ACA marketplace enrollees will be subjected to new verification rules requiring revalidation of eligibility. In addition, repayment caps for excess subsidies will be eliminated and the enhanced ACA subsidies are set to expire after 2025.

- Other impending healthcare changes include the eligibility of more ACA marketplace plans for Health Savings Accounts (HSAs) and modifications to Medicare drug price negotiation rules.

- The majority of these changes are set to take effect between 2026 and 2028.

How the One Big Beautiful Bill Act Reshapes Health Insurance

The OBBBA brings sweeping alterations to how individuals secure and maintain health insurance, most notably in Medicaid and ACA marketplace coverage. Medicaid is a joint federal-state initiative offering free or cost-effective health coverage to over 70 million low-income individuals, elderly, children, and people with disabilities, while ACA marketplace coverage pertains to private health insurance plans that people purchase via HealthCare.gov or state exchanges, often including income-based premium tax credits.

According to predictions from health policy researchers and federal budget analysts, the insurance-related provisions of the law could result in millions of people losing coverage over the next decade. The largest impacts are expected from new Medicaid work requirements, tougher eligibility and verification rules, and the end of enhanced ACA subsidies.

Impacts estimated by the Congressional Budget Office and other health policy researchers include:

- Medicaid work requirements: Over 5 million people could lose health insurance by 2034 due to new work and reporting requirements.

- Intensified eligibility checks: Around 700,000 people may lose Medicaid coverage because some enrollees will need to verify eligibility every six months instead of annually.

- Expiration of enhanced ACA subsidies: Approximately 22 million people, including 5 million small-business owners and self-employed workers, could face increased marketplace premiums in 2026 if enhanced subsidies expire as scheduled.

- Loss of marketplace coverage: Almost 4.2 million people could become uninsured by 2034 if ACA coverage becomes unaffordable.

Several of the health insurance modifications in the OBBBA will come into force from 2026 to 2028.

Major Healthcare Changes in the One Big Beautiful Bill Act

The provisions of the law impact consumers in different ways. While some changes directly affect coverage eligibility and out-of-pocket expenses, others alter the operation of specific programs and benefits. Here are the most significant, consumer-facing healthcare changes in the law:

1. Medicaid Work Requirements

The law mandates that adults aged 19 to 64 enrolled in the Medicaid expansion program must complete at least 80 hours of work or community engagement activities each month to retain their coverage. Verification of compliance must be carried out by states at least twice per year. Failure to meet these requirements could lead to loss of Medicaid coverage, even for those who qualify based on income.

There are mandatory exemptions in the law for certain groups such as medically frail individuals, disabled veterans, pregnant individuals, and certain caregivers. However, qualifying for an exemption may still require the submission of paperwork or documentation to confirm their status.

States that expanded Medicaid under the ACA must implement these rules by January 1, 2027, although they may choose to adopt them earlier. Only Georgia has a Medicaid work requirement in effect, as it launched its program in 2023 under a federal waiver.

2. Medicaid Cost-Sharing Copays Up To $35 Per Visit

Adults in the Medicaid expansion program may be required to pay copays of up to $35 per visit for certain services. This marks the first instance where Medicaid enrollees may have regular cost sharing for covered care. However, the total cost sharing is capped at 5% of household income, thereby limiting the overall amount enrollees can pay.

Certain services, including primary care, prescription medications, and rural health clinic services among others, remain exempt from this rule.

3. Stricter Verification Rules For ACA Marketplace Subsidies

Individuals who receive ACA premium tax credits are required to complete pre-enrollment verification before coverage commences. This process necessitates advance confirmation of income and eligibility, as opposed to post-enrollment verification.

This could lead to limitations on automatic reenrollment for some marketplace enrollees, which may require them to revalidate their eligibility or reapply annually to retain their subsidies.

4. Removal Of Cap On Excess ACA Subsidy Repayment

ACA marketplace health insurance costs can be lowered with premium tax credits for people with moderate incomes. These subsidies can be paid in advance to lower monthly premiums (in the form of advance premium tax credits), or claimed later on a tax return.

With the introduction of the new law, there’s no longer a limit on the repayment of any excess advance premium tax credit if an enrollee’s income turns out to be higher than anticipated. While repayment caps previously applied to households earning under 400% of the federal poverty level, these caps will be removed starting in 2026.

5. Restrictions on Medicare Eligibility For Certain Individuals

The law alters the eligibility criteria for Medicare, restricting access for some previously qualified noncitizens. Under the revised rules, enrollment in Medicare is limited to certain immigration categories, reducing the pool of potential enrollees.

More Medicare-related changes, including delays to enrollment assistance programs and updates to drug price negotiation rules, are further discussed below.

6. Enhancements to Tax-Advantaged Accounts

The dependent care flexible spending account (FSA) contribution limit will be increased from $5,000 to $7,500 per household from 2026. FSAs allow employees to use pretax dollars for eligible child care or dependent care expenses like daycare or after-school care. However, the increased limit is applicable only if an employer modifies its plan design to permit increased contributions.

Additionally, the law expands access to health savings accounts (HSAs). HSAs are tax-advantaged savings accounts that let people with eligible high-deductible health plans (HDHPs) set aside money for medical expenses. These contributions, made with pretax dollars, grow tax-free and can be withdrawn tax-free when used for eligible healthcare costs.

Under the new legislation, more people are permitted to use HSAs to save for medical expenses with tax advantages as bronze and catastrophic ACA marketplace plans now qualify as HSA-eligible plans.

Does the Big Beautiful Bill Act Include Medicare Cuts?

Wide-ranging healthcare cuts to Medicaid and ACA indirectly affect many Medicare beneficiaries, including those who are eligible for both Medicare and Medicaid. Here are some provisions that could limit or reduce certain types of Medicare support:

1. Postponement of Improvements to Medicare Savings Program

The Medicare Savings Program (MSP) helps people with lower incomes pay for Medicare costs such as premiums, deductibles, and coinsurance. A 2023 rule by the Centers for Medicare & Medicaid Services was slated to streamline MSP enrollment and eligibility processes, lessen administrative burdens, and make it easier for individuals to retain their coverage. However, the OBBBA postponed the implementation of this rule until 2034.

2. New Medicare Eligibility Requirements

The OBBBA revises the eligibility criteria for Medicare. Prior to this law, many legally present immigrants could qualify for Medicare if they worked and paid payroll taxes for a sufficient period, or if they met certain eligibility rules. However, under the new law, only specific groups, including U.S. citizens, lawful permanent residents (green card holders), Cuban and Haitian entrants, and individuals from certain Pacific Island nations with special arrangements with the U.S., can register for Medicare.

Groups that can no longer register for Medicare include refugees and people granted asylum, people with Temporary Protected Status, survivors of human trafficking, survivors of domestic violence, individuals granted humanitarian parole, among others.

By July 2026, the Social Security Administration is required to identify people who currently have Medicare but do not meet the new immigration rules. These individuals will be notified that their Medicare coverage will end in January 2027.

3. Restriction on Medicare Drug Price Negotiation

The Inflation Reduction Act of 2022 provided Medicare with the power to negotiate prices for some high-cost prescription drugs. However, an exception was made for orphan drugs, medicines used to treat rare conditions that affect fewer than 200,000 people in the United States. For these medications, exemption from price negotiations was only granted if they were approved to treat one rare condition.

However, if a second rare condition was researched for its orphan drug, that drug could become subject to negotiation. As a result, some manufacturers slowed or stopped research into new uses. A report by the National Pharmaceutical Council found that approval for multiple conditions for orphan drugs was halved following the enactment of the Inflation Reduction Act.

The new law expands the orphan drug exemption. It allows orphan drugs approved for one or more rare-condition indications to remain exempt from Medicare price negotiations. These changes apply to Medicare drug prices beginning on January 1, 2028.

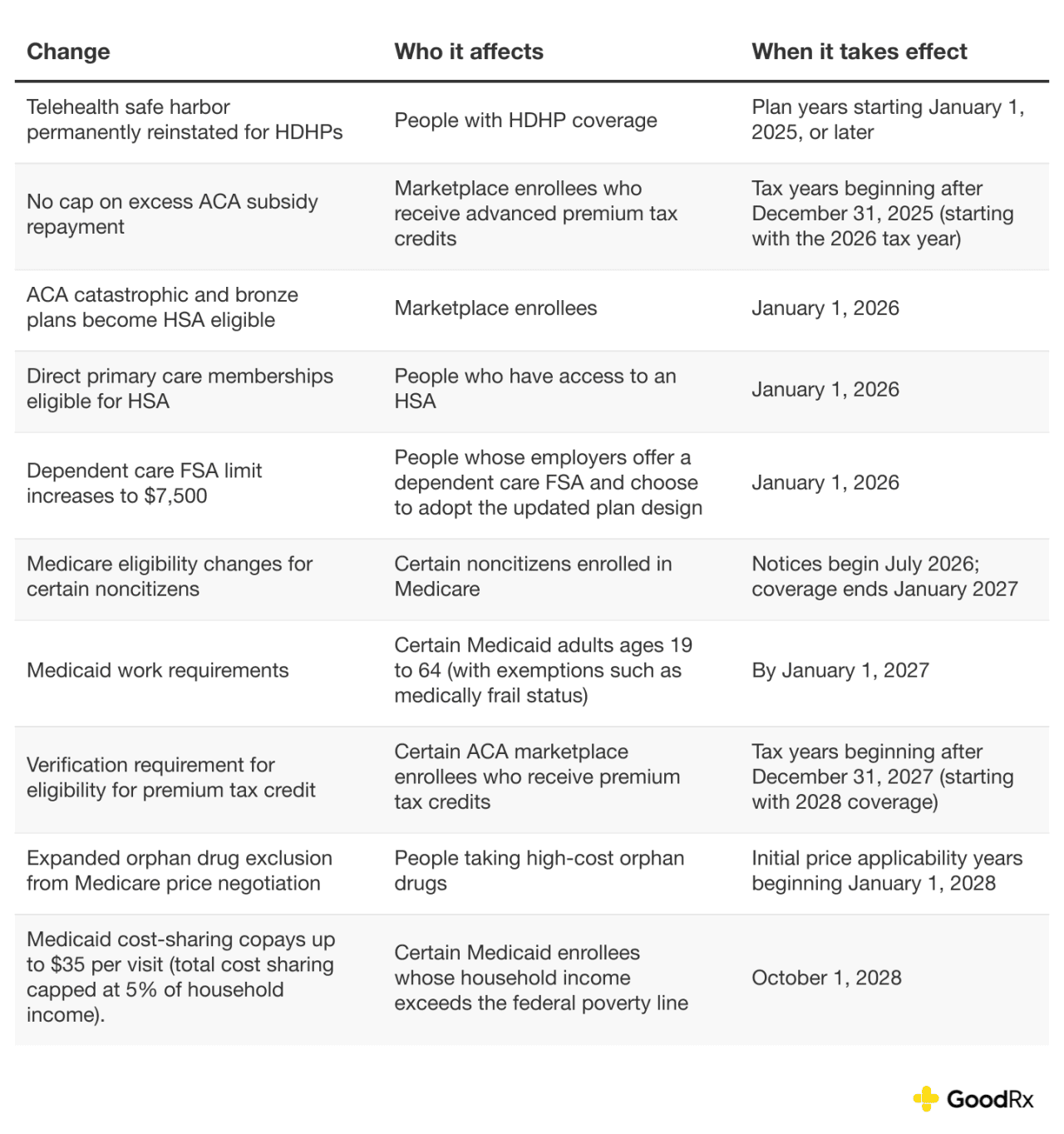

Implementation Timeline for the Big Beautiful Bill Act Healthcare Changes

The timeline below highlights the effective dates for the major healthcare changes highlighted in this article, along with a few health-related provisions in the OBBBA:

GoodRx

GoodRx

Final Thoughts

The One Big Beautiful Bill ushers in numerous changes to healthcare, affecting Medicaid, Medicare, and the Affordable Care Act marketplace. While some individuals may face higher premiums and new rules to maintain enrollment, others may find increased flexibility with their tax-advantaged health accounts, such as health savings accounts and dependent care flexible spending accounts.

Being aware of when these changes come into effect can assist you in preparing for open enrollment and avoiding unexpected healthcare costs.

This information was sourced from this story written by GoodRx and distributed and reviewed by Stacker.

“`

—

Read More US Economic News